Understanding Form 706 and Protecting Your Family’s Wealth

Two things in life are certain: death and taxes. For families with significant assets, those two realities collide in a very real way through Form 706, the Federal Estate Tax Return.

If your estate approaches or exceeds the federal exemption, around $15 million in 2026, this filing becomes one of the most important financial and legal events your family will face. Done correctly, it preserves wealth. Done poorly, it can trigger taxes, penalties, and unnecessary loss of assets.

Understanding the Dual Tax System

Form 706 is not just about one tax. It addresses two separate but connected systems:

Estate Tax

Applies when the total value of the estate, combined with prior taxable gifts, exceeds the federal exemption.

Generation Skipping Transfer Tax

Applies to transfers made to grandchildren or beneficiaries more than one generation below the decedent.

Both share the same exemption amount, but they must be tracked and reported carefully. A mistake in allocating exemptions, especially GST exemption, can result in a 40 percent tax that could have been avoided entirely.

Why Form 706 Matters Even Below the Exemption

Many families assume that if their estate is below the exemption, they do not need to file. That is not always true.

One of the most valuable benefits in estate tax law is portability, which allows a surviving spouse to use the unused exemption of the deceased spouse. This is known as the DSUE.

If Form 706 is not properly filed, that unused exemption is lost. That mistake alone can cost a family millions in future tax exposure.

The Complexity Behind the Filing

Form 706 is not a simple tax return. It is a comprehensive financial snapshot of everything a person owned at death.

This includes:

- Real estate

- Closely held businesses

- Investment accounts and securities

- Life insurance proceeds

- Retirement accounts

- Digital assets

Each asset must be reported at fair market value, often requiring formal appraisals.

Even estates that are filing “just for portability” must complete the return accurately. Missing schedules, incorrect valuations, or incomplete disclosures can invalidate the entire filing.

Critical Deadlines You Cannot Miss

Timing is one of the biggest pressure points.

- Filing deadline: 9 months from date of death

- Extension available: Up to 6 additional months by filing Form 4768

- Payment deadline: Still due at 9 months, even with an extension

For smaller estates seeking portability only, IRS relief may allow filing up to five years after death, but only if the return is properly prepared and meets strict requirements.

The Liquidity Problem Most Families Face

One of the biggest challenges is not calculating the tax. It is paying it.

Estate taxes are due in cash, even if most of the estate is tied up in illiquid assets like:

- Family businesses

- Real estate

- Private investments

Without planning, families may be forced to sell assets quickly, often at reduced value, just to meet the tax obligation.

Options to Manage the Tax Burden

There are limited but important relief tools available:

Section 6161

Allows an extension of time to pay if there is reasonable cause or hardship, but interest still accrues.

Section 6166

Allows installment payments over time for estates with significant closely held business interests.

These options can help, but they require proper planning and qualification.

Planning Ahead to Avoid Forced Sales

The best strategy is proactive planning.

Common tools include:

- Life insurance held in an irrevocable trust to create tax-free liquidity

- Structuring business ownership to qualify for installment payment options

- Coordinating trusts to maximize exemptions and timing

Without planning, families are often forced into selling businesses or real estate under pressure. With planning, those assets can remain intact.

Common Mistakes That Create Big Problems

Errors on Form 706 can have long-term consequences:

- Losing portability due to improper filing

- Incomplete or missing schedules

- Incorrect valuations

- Misallocation of deductions

- Failure to coordinate with income tax filings

These mistakes often lead to audits, penalties, and unnecessary legal costs.

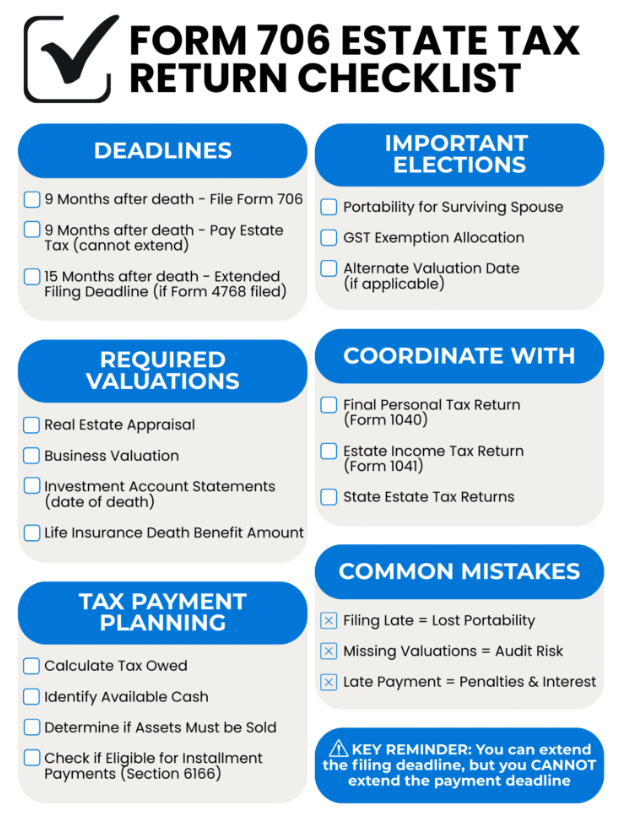

Form 706 Filing Checklist

Before Filing

- Obtain an EIN for the estate

- Gather all asset information and valuations

- Compile lifetime gift history

- Review beneficiary designations and titling

Key Deadlines

- Track the 9 month filing deadline

- Track the 9 month payment deadline

- Evaluate eligibility for extensions or portability relief

Valuation Requirements

- Appraisals for real estate and businesses

- Date of death values for securities

- Insurance and retirement account documentation

Coordination

- Align with final individual income tax return

- Coordinate with estate income tax return

- Properly allocate deductions

Liquidity Planning

- Estimate total tax liability

- Identify available cash or liquid assets

- Evaluate payment options and timelines

Key Elections

- Portability election

- Alternate valuation date

- GST exemption allocation

- Marital trust elections

The Bottom Line

Form 706 is one of the most complex and high stakes filings your family may ever face. It sits at the intersection of tax law, valuation, and estate planning strategy.

Handled correctly, it protects generational wealth. Handled poorly, it can erode it quickly.

Work With Cavalier Law Group

At Cavalier Law Group, we help families in Southwest Ranches, Weston, Davie, Cooper City, Sunrise, and Pembroke Pines plan ahead so Form 706 is not a reactive scramble but part of a coordinated strategy. We work alongside your financial and tax advisors to ensure your estate is structured for efficiency, liquidity, and long term protection.

If your estate may be approaching federal thresholds or includes business interests, real estate, or complex assets, now is the time to plan, not later.

Disclaimer

This content is for informational purposes only and does not constitute legal or tax advice. Reading this material does not create an attorney client relationship. Federal and state laws are subject to change and may vary based on individual circumstances. You should consult with a qualified attorney and tax professional regarding your specific situation before making any decisions.